Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Home prices post strongest annual gain in nearly 8 years

Home prices in most metropolitan areas grew significantly in the third quarter, with the national median price rising at its fastest annual clip in nearly eight years, according to the National Association of Realtors (NAR).

During the same period, existing homes sold at the fastest annual rate recorded in more than six years, according to NAR’s latest quarterly report on metro area median prices and affordability.

Despite the robust price growth, NAR estimated that potential buyers still had adequate income in most areas to purchase a home in the third quarter. Nonetheless, market momentum is changing, according to Lawrence Yun, chief economist at NAR.

“Rising prices and higher interest rates have taken a bite out of housing affordability,” Yun said. “However, we have the ongoing situation of more buyers than sellers in the market, so lower sales will help to take the pressure off home price growth and allow them to rise slowly at a single-digit growth rate in 2014.”

The national median existing single-family home price increased by 12.5 percent year over year to $207,300 in the third quarter, the strongest year-over-year gain since the fourth quarter of 2005 when it shot up 13.6 percent, according to the trade group.

In the second quarter, the median price reportedly rose 12.2 percent year over year.

– See more at: http://www.inman.com/2013/11/06/home-prices-post-highest-annual-gain-in-nearly-8-years/#!

Home prices in most metropolitan areas grew significantly in the third quarter, with the national median price rising at its fastest annual clip in nearly eight years, according to the National Association of Realtors (NAR).

During the same period, existing homes sold at the fastest annual rate recorded in more than six years, according to NAR’s latest quarterly report on metro area median prices and affordability.

Despite the robust price growth, NAR estimated that potential buyers still had adequate income in most areas to purchase a home in the third quarter. Nonetheless, market momentum is changing, according to Lawrence Yun, chief economist at NAR.

“Rising prices and higher interest rates have taken a bite out of housing affordability,” Yun said. “However, we have the ongoing situation of more buyers than sellers in the market, so lower sales will help to take the pressure off home price growth and allow them to rise slowly at a single-digit growth rate in 2014.”

The national median existing single-family home price increased by 12.5 percent year over year to $207,300 in the third quarter, the strongest year-over-year gain since the fourth quarter of 2005 when it shot up 13.6 percent, according to the trade group.

In the second quarter, the median price reportedly rose 12.2 percent year over year.

– See more at: http://www.inman.com/2013/11/06/home-prices-post-highest-annual-gain-in-nearly-8-years/#!

Home prices in most metropolitan areas grew significantly in the third quarter, with the national median price rising at its fastest annual clip in nearly eight years, according to the National Association of Realtors (NAR).

During the same period, existing homes sold at the fastest annual rate recorded in more than six years, according to NAR’s latest quarterly report on metro area median prices and affordability.

Despite the robust price growth, NAR estimated that potential buyers still had adequate income in most areas to purchase a home in the third quarter. Nonetheless, market momentum is changing, according to Lawrence Yun, chief economist at NAR.

“Rising prices and higher interest rates have taken a bite out of housing affordability,” Yun said. “However, we have the ongoing situation of more buyers than sellers in the market, so lower sales will help to take the pressure off home price growth and allow them to rise slowly at a single-digit growth rate in 2014.”

The national median existing single-family home price increased by 12.5 percent year over year to $207,300 in the third quarter, the strongest year-over-year gain since the fourth quarter of 2005 when it shot up 13.6 percent, according to the trade group.

In the second quarter, the median price reportedly rose 12.2 percent year over year.

– See more at: http://www.inman.com/2013/11/06/home-prices-post-highest-annual-gain-in-nearly-8-years/#!

Home prices in most metropolitan areas grew significantly in the third quarter, with the national median price rising at its fastest annual clip in nearly eight years, according to the National Association of Realtors (NAR).

During the same period, existing homes sold at the fastest annual rate recorded in more than six years, according to NAR’s latest quarterly report on metro area median prices and affordability.

Despite the robust price growth, NAR estimated that potential buyers still had adequate income in most areas to purchase a home in the third quarter. Nonetheless, market momentum is changing, according to Lawrence Yun, chief economist at NAR.

“Rising prices and higher interest rates have taken a bite out of housing affordability,” Yun said. “However, we have the ongoing situation of more buyers than sellers in the market, so lower sales will help to take the pressure off home price growth and allow them to rise slowly at a single-digit growth rate in 2014.”

The national median existing single-family home price increased by 12.5 percent year over year to $207,300 in the third quarter, the strongest year-over-year gain since the fourth quarter of 2005 when it shot up 13.6 percent, according to the trade group.

In the second quarter, the median price reportedly rose 12.2 percent year over year.

– See more at: http://www.inman.com/2013/11/06/home-prices-post-highest-annual-gain-in-nearly-8-years/#!

Home prices in most metropolitan areas grew significantly in the third quarter, with the national median price rising at its fastest annual clip in nearly eight years, according to the National Association of Realtors (NAR).

During the same period, existing homes sold at the fastest annual rate recorded in more than six years, according to NAR’s latest quarterly report on metro area median prices and affordability.

Despite the robust price growth, NAR estimated that potential buyers still had adequate income in most areas to purchase a home in the third quarter. Nonetheless, market momentum is changing, according to Lawrence Yun, chief economist at NAR.

“Rising prices and higher interest rates have taken a bite out of housing affordability,” Yun said. “However, we have the ongoing situation of more buyers than sellers in the market, so lower sales will help to take the pressure off home price growth and allow them to rise slowly at a single-digit growth rate in 2014.”

The national median existing single-family home price increased by 12.5 percent year over year to $207,300 in the third quarter, the strongest year-over-year gain since the fourth quarter of 2005 when it shot up 13.6 percent, according to the trade group.

In the second quarter, the median price reportedly rose 12.2 percent year over year.

– See more at: http://www.inman.com/2013/11/06/home-prices-post-highest-annual-gain-in-nearly-8-years/#!

Home prices in most metropolitan areas grew significantly in the third quarter, with the national median price rising at its fastest annual clip in nearly eight years, according to the National Association of Realtors (NAR).

During the same period, existing homes sold at the fastest annual rate recorded in more than six years, according to NAR’s latest quarterly report on metro area median prices and affordability.

Despite the robust price growth, NAR estimated that potential buyers still had adequate income in most areas to purchase a home in the third quarter. Nonetheless, market momentum is changing, according to Lawrence Yun, chief economist at NAR.

“Rising prices and higher interest rates have taken a bite out of housing affordability,” Yun said. “However, we have the ongoing situation of more buyers than sellers in the market, so lower sales will help to take the pressure off home price growth and allow them to rise slowly at a single-digit growth rate in 2014.”

The national median existing single-family home price increased by 12.5 percent year over year to $207,300 in the third quarter, the strongest year-over-year gain since the fourth quarter of 2005 when it shot up 13.6 percent, according to the trade group.

In the second quarter, the median price reportedly rose 12.2 percent year over year.

– See more at: http://www.inman.com/2013/11/06/home-prices-post-highest-annual-gain-in-nearly-8-years/#!

Home prices in most metropolitan areas grew significantly in the third quarter, with the national median price rising at its fastest annual clip in nearly eight years, according to the National Association of Realtors (NAR).

During the same period, existing homes sold at the fastest annual rate recorded in more than six years, according to NAR’s latest quarterly report on metro area median prices and affordability.

Despite the robust price growth, NAR estimated that potential buyers still had adequate income in most areas to purchase a home in the third quarter. Nonetheless, market momentum is changing, according to Lawrence Yun, chief economist at NAR.

“Rising prices and higher interest rates have taken a bite out of housing affordability,” Yun said. “However, we have the ongoing situation of more buyers than sellers in the market, so lower sales will help to take the pressure off home price growth and allow them to rise slowly at a single-digit growth rate in 2014.”

The national median existing single-family home price increased by 12.5 percent year over year to $207,300 in the third quarter, the strongest year-over-year gain since the fourth quarter of 2005 when it shot up 13.6 percent, according to the trade group.

In the second quarter, the median price reportedly rose 12.2 percent year over year.

– See more at: http://www.inman.com/2013/11/06/home-prices-post-highest-annual-gain-in-nearly-8-years/#!

Pace of sales hits 5.36M a year during third quarter, best since 2007

Home prices in most metropolitan areas grew significantly in the third quarter, with the national median price rising at its fastest annual clip in nearly eight years, according to the National Association of Realtors (NAR).

During the same period, existing homes sold at the fastest annual rate recorded in more than six years, according to NAR’s latest quarterly report on metro area median prices and affordability.

Despite the robust price growth, NAR estimated that potential buyers still had adequate income in most areas to purchase a home in the third quarter. Nonetheless, market momentum is changing, according to Lawrence Yun, chief economist at NAR.

“Rising prices and higher interest rates have taken a bite out of housing affordability,” Yun said. “However, we have the ongoing situation of more buyers than sellers in the market, so lower sales will help to take the pressure off home price growth and allow them to rise slowly at a single-digit growth rate in 2014.”

The national median existing single-family home price increased by 12.5 percent year over year to $207,300 in the third quarter, the strongest year-over-year gain since the fourth quarter of 2005 when it shot up 13.6 percent, according to the trade group.

In the second quarter, the median price reportedly rose 12.2 percent year over year.

Meanwhile, NAR said existing-home sales jumped 5.9 percent to a seasonally adjusted annual rate of 5.36 million in the third quarter from 5.06 million in the second quarter.

On an annual basis, they reportedly increased 13 percent. The third-quarter pace of sales was the highest recorded since the first quarter of 2007, when it hit 5.66 million, NAR said.

The report’s findings also highlighted the market’s sharp inventory shortage.

At the rate of sales in the third quarter, the existing-home inventory of 2.21 million homes for sale would have cleared in just five months, down from 5.9 months in the third quarter of 2012.

Are you curious what your home might be worth? Give us a call, text or email. We'ed be to provided you with a comparative market analysis of your home, condominum or multi-family home.

-Steve and Sandra

Steve Hill and Sandra Brenner

Windermere Real Estate/FN

Seattle-Northwest

122502 Greenwood Ave N

Seattle WA 98133

call/text: 206-769-9577

email: stevehill@windermere.com

Check out these useful links:

BrennerHill.com

Best In Client Satisfaction

Windermere Housing Trends Newsletter

Our Preferred Lenders

George Runnels

Washington First Mortgage

WaFirstMortgage.com

call/text: 206-604-4545

Jackie Murphy

Cobalt Mortgage

CobaltMortgage.com

call/text: 425-260-6834

How to Set Your Selling Price

Being overpriced is a bad start

Being overpriced is a bad start

If you're selling your house, one of the first steps you'll take is setting an asking price, a maneuver that requires the ability to find the perfect balance between attracting solid offers and ultimately receiving top dollar.

- Upgrades have been added. While many home improvements will help you recoup a good chunk of your investment, it won't give you 100 percent of what you paid. Also, the more personal the improvement—a swimming pool, a sunroom, purple floors—the less likely it will be viewed favorably by potential buyers.

- The need for money.

- You're moving to a higher-priced area.

- The original purchase price was too high.

- The seller lacks factual comparable sales to prove what the market value is.

- The seller wants bargaining room (listing more than 1-3 percent above market value actually reduces bargaining power).

- An unnecessary move, so you're not motivated.

Steve Hill and Sandra Brenner

Windermere Real Estate/FN

Seattle – Northwest

122502 Greenwood Ave N

Seattle WA 98133

call/text: 206-769-9577

email: stevehill@windermere.com

Check out these useful links:

BrennerHill.com

Best In Client Satisfaction

Windermere Housing Trends Newsletter

Our Preferred Lenders

George Runnels

Washington First Mortgage

WaFirstMortgage.com

call/text: 206-604-4545

Jackie Murphy

Cobalt Mortgage

CobaltMortgage.com

call/text: 425-260-6834

FSBO’s Must Be Ready to Negotiate

In a recovering market, some sellers might be tempted to try and sell their home on their own (FSBO) without using the services of a real estate professional. The real estate agent is a trained and experienced negotiator. In most cases, the seller is not. The seller must realize the ability to negotiate will determine whether they get the best deal for themselves and their family.

In a recovering market, some sellers might be tempted to try and sell their home on their own (FSBO) without using the services of a real estate professional. The real estate agent is a trained and experienced negotiator. In most cases, the seller is not. The seller must realize the ability to negotiate will determine whether they get the best deal for themselves and their family.

Here is a list of some of the people with whom the seller must be prepared to negotiate if they decide to FSBO:

- The buyer who wants the best deal possible

- The buyer’s agent who solely represents the best interest of the buyer

- The buyer’s attorney (in some parts of the country)

- The home inspection companies which work for the buyer and will almost always find some problems with the house.

- The termite company if there are challenges

- The buyer’s lender if the structure of the mortgage requires the sellers’ participation

- The appraiser if there is a question of value

- The title company if there are challenges with certificates of occupancy (CO) or other permits

- The town or municipality if you need to get the Cos permits mentioned above

- The buyer’s buyer in case there are challenges on the house your buyer is selling.

- Your bank in the case of a short sale

If you are looking for a skilled negotiator to help you purchase or sell a home, give us a call, text or email; we would love to put our experience to work for you!

?-Steve and Sandra

Steve Hill and Sandra Brenner

Windermere Real Estate/FN

122502 Greenwood Ave N

Seattle WA 98133

call/text: 206-769-9577

email: stevehill@windermere.com

Check out these useful links:

BrennerHill.com

Best In Client Satisfaction

Windermere Housing Trends Newsletter

Our Preferred Lenders

George Runnels

Washington First Mortgage

WaFirstMortgage.com

call/text: 206-604-4545

Jackie Murphy

Cobalt Mortgage

CobaltMortgage.com

call/text: 425-260-6834

Seattle View Home Sale

Beautiful Seattle contmporary home for sale in Seattle's coveted North Beach neighborhood.

Open Saturday

November 9th

1PM-4PM

Custom built home is tucked away in North Beach w/ modern lines, perfectly situated on a private lot w/ sound views. High end materials & quality craftsmanship throughout. Light filled & open floor plan w/ a seamless flow to outdoor living. Two story entry. Top of the line kitchen w/ slab granite counters, ss package, gas cooking & a huge island w/ sit-up eating. Spa-like master bedroom w/ palatial bath. Work out room. Wine cellar. Custom built-ins + lots of thoughtful extras at every turn.

Stop by Saturday to see this great home.

If you are looking for something different, let us know. We are experts for North Seattle view neighborhoods. Give us a call, text or email. and put our experieince and negotiating skills to work for you!

?-Steve and Sandra

Steve Hill and Sandra Brenner

Windermere Real Estate/FN

122502 Greenwood Ave N

Seattle WA 98133

call/text: 206-769-9577

email: stevehill@windermere.com

Check out these useful links:

BrennerHill.com

Best In Client Satisfaction

Windermere Housing Trends Newsletter

Our Preferred Lenders

George Runnels

Washington First Mortgage

WaFirstMortgage.com

call/text: 206-604-4545

Jackie Murphy

Cobalt Mortgage

CobaltMortgage.com

call/text: 425-260-6834?

Five things to know about buying a fixer-upper

So you’re buying a fixer-upper? The house looks good, needs some work and is in a desirable neighborhood. But what might seem like a great fixer-upper property could actually be a money pit. Let’s look at some common potential issues with a home that could easily derail an appraisal and your mortgage.

Here are some common red flags that could halt your loan – and they come up more frequently than one might think. And just a note: It’s all about the appraisal and contract. If the problem isn’t listed in the appraisal or listed as a condition of sale within the purchase contract, it shouldn’t delay or deny your loan.

Roof

Many resale homes have worn-out roofs that must be replaced at some point down the road, some much sooner than others. In this situation, your real estate agent is bound to identify it right upfront. Get at least a couple of quotes to determine how much shelf life the roof actually has, and the costs associated with repairing or replacing the roof if need be. If the roof is shot (or worse — has a leak), and it’s identified in the appraisalas “subject to condition,” it will have to be fixed in accordance with the appraiser’s comments. It will also mean a second visit from the appraiser to sign off on the completion of the repair.

Open Subfloor

This one is biggie. Open and exposed subflooring is an automatic red flag because it presents a potential health and safety concern for the buyer of the property. As such, this is guaranteed to stop the loan, and the appraiser will be mandated to notate it in the appraisal as a condition that needs to be satisfied to make the property lendable

Exposed Wiring

This seems obvious, right? Well, in many cases homes have exposed wiring either on the exterior or the interior of the home, which poses — you guessed it — another health and safety concern. It would be best to repair any exposed wiring prior to the appraiser visiting the property for the first time.

Dry Rot

Whether or not a rotten area is viewed as a condition of hazard depends on the individual appraiser. In most cases, appraisers simply want a rotted area repaired to make an appraisal clean — and also to cover their backside, so to speak.

Pest Damage

If there is large-scale pest damage — for example, if any average Joe can see obvious termite or pest damage when viewing the home — then yes, it’s probably going to be need to be fixed. However, it’s more common to see it identified as a condition of sale in the real estate purchase contract — at which point it must be fixed.

Who Pays for the Repairs When Buying a Fixer-Upper?

Such repairs could be paid for by buyer, seller, listing agent or buyer’s agent. More commonly, the buyer typically pays for such repairs to the property, but this is always negotiable. It can be paid by any one of these parties, even be split multiple ways.

As an informed home buyer, you’d want to make sure your loan is approved with the lender prior to making any repairs. The last thing you want to deal with is fixing repairs on a property you don’t own yet when you’re loan hasn’t been signed off.

There are other repairs that inevitably come up when looking at properties, including the property needing a CO2 detector (which is a law in many states), obvious repairs such as broken windows or an unstable deck are all examples of health and safety concerns. It’s not the lender that delays the loan in these situations. Rather, it’s the scope of the repairs as notated by the appraiser, as well at the time it takes to have those items repaired, that can slow down the lending process.

Whatever the case may be, proactively communicating with your mortgage lender and real estate agent about any repairs that need to be done is the best course of action to take to ensure the financing for your purchase comes through.

Have other questions about investing in a home? Give us a call, text or email, we would love to answer any questions you may have.

?-Steve and Sandra

Steve Hill and Sandra Brenner

Windermere Real Estate/FN

122502 Greenwood Ave N

Seattle WA 98133

call/text: 206-769-9577

email: stevehill@windermere.com

Check out these useful links:

BrennerHill.com

Best In Client Satisfaction

Windermere Housing Trends Newsletter

Our Preferred Lenders

George Runnels

Washington First Mortgage

WaFirstMortgage.com

call/text: 206-604-4545

Jackie Murphy

Cobalt Mortgage

CobaltMortgage.com

Millennials: Your Time Is Now

Our guest blogger today is Justin DeCesare. Justin is the CEO of Middleton & Associates Real Estate and has some great advice for the Millennial generation in today's post.

Our guest blogger today is Justin DeCesare. Justin is the CEO of Middleton & Associates Real Estate and has some great advice for the Millennial generation in today's post.

There will likely be no other time in the lifespan of the Millennial generation that is filled with more opportunity than right now.

I understand that the preceding sentence may seem overly optimistic, but when we look at modern history, all generations flourished more in the decade following an economic downturn than any other.

This, coupled with exponential growth in technology, is currently paving the way for a wave of young entrepreneurs and successful business people unparalleled in our Millennial Timeline.

Generally, I write these blogs to help instill the importance of our generation to Real Estate Agents and Brokers, but today, my message is directly to you, the young Millennial Yourself.

If you have not already grasped the importance that the next five years are going to have on your life, do so today.

Get Pumped Up.

This isn’t high school anymore, and our teenage-angst should have been thrown by the wayside along with every other burdensome baggage we have carried along the way.

Prices are at their lowest, NOW

Economists around the country agree that housing prices have fallen to their true lows, corrected, and should now be back on track for the steady growth necessary to maintain a healthy market.

New housing inventory is minimal, and EVENTUALLY the government will be forced to curtail bond buying programs, and as monetary policy is contracted the price of borrowing will increase.

By far the greatest reason you have to buy a home NOW and not 2 years from now is that money is cheap… cheaper than it has ever been and cheaper than it will ever be.

Stop Renting!

Plus, when you are renting, you are throwing your money away in taxes, especially those single professionals who have no other write-offs.

I am a Millennial. I am 30. I bought my first home when I was 21 while I was enlisted in the Navy. My mindset has changed over the last 10 years, but I can say this: Youthful optimism may be the best asset we have. At 21, fear of failing and needing to start over with kids’ college funds to worry about do not weigh as heavily as they will 10 years from now.

Your jobs are starting to come back. With every tepid job report comes the chance for new jobs to be found that pay in line with what you are worth.

Take advantage of this time and don’t look back in 25 years saying, “It really was the best opportunity of my life.”

This is your opportunity for freedom, your opportunity to own something that gives back, and doesn’t merely suck the value out of your debit card.

Are you ready to invest in your future? Let us help you find the investment that works best for you. Give us a call, text or email today.

?-Steve and Sandra

Steve Hill and Sandra Brenner

Windermere Real Estate/FN

122502 Greenwood Ave N

Seattle WA 98133

call/text: 206-769-9577

email: stevehill@windermere.com

Check out these useful links:

BrennerHill.com

Best In Client Satisfaction

Windermere Housing Trends Newsletter

Our Preferred Lenders

George Runnels

Washington First Mortgage

WaFirstMortgage.com

call/text: 206-604-4545

Jackie Murphy

Cobalt Mortgage

CobaltMortgage.com

call/text: 425-260-6834

Five Evergreen State cities placed in the top-100 best places to live in the U.S

Bellevue, Bellingham, Tacoma, Redmond, Everett and Vancouver WA were all named in the top 500 best places to live in the US. Check out the article HERE

Bellevue, Bellingham, Tacoma, Redmond, Everett and Vancouver WA were all named in the top 500 best places to live in the US. Check out the article HERE

If you are considering a move to any of these top 500 cities, give us a call, we have an exceptional referral network of brokers and agents throught the Untied States.

-Steve and Sandra

Steve Hill and Sandra Brenner

Windermere Real Estate/FN

122502 Greenwood Ave N

Seattle WA 98133

call/text: 206-769-9577

email: stevehill@windermere.com

Check out these useful links:

BrennerHill.com

Best In Client Satisfaction

Windermere Housing Trends Newsletter

Our Preferred Lenders

George Runnels

Washington First Mortgage

WaFirstMortgage.com

call/text: 206-604-4545

Jackie Murphy

Cobalt Mortgage

CobaltMortgage.com

call/text: 425-260-6834

?

Why You Should Sell Your House Now

Many now realize that it is a great time to buy a home. It might also be an opportune time to sell your house. Here are the five reasons we believe now may be a perfect time to put your house on the market.

Many now realize that it is a great time to buy a home. It might also be an opportune time to sell your house. Here are the five reasons we believe now may be a perfect time to put your house on the market.

1. Demand Is High

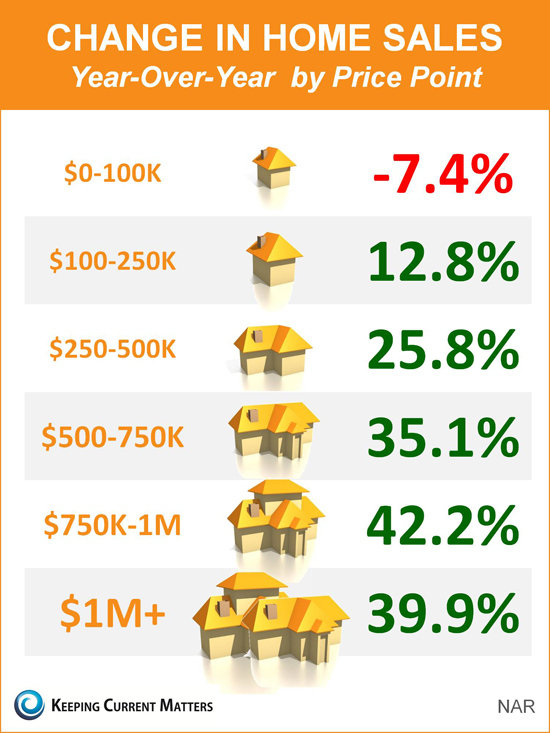

The most recent Existing Home Sales Reports by the National Association of Realtors (NAR) show a double digit percent increase in sales year-over year; sales have remained above last year’s levels for over 25 months. There are buyers out there right now and they are serious about purchasing.

2. Supply Is Beginning to Increase

Total housing inventory is again approaching historic norms of a 5 month supply compared with 4.3 months in January. Many expect inventory to continue to rise as 3.2 million homeowners escaped the shackles of negative equity in the last 12 months and an additional 1.9 million are expected to enter positive equity in the next 12 months. Selling now while demand is high and before supply increases may garner you your best price.

3. New Construction Is Coming Back

Over the last several years, most homeowners selling their home did not have to compete with a new construction project around the block. As the market is recovering, more and more builders are jumping back in. These ‘shiny’ new homes will again become competition as they are an attractive alternative for many purchasers.

4. Interest Rates Will Again Rise

Although Freddie Mac’s Primary Mortgage Market Survey shows that interest rates for a 30-year mortgage have softened recently, most experts predict that they will begin to rise later this year. The Mortgage Bankers Association, Fannie Mae, Freddie Mac and the National Association of Realtors are in unison projecting that rates will be up almost a full percentage point by this time next year.

Whether you are moving up or moving down, your housing expense will be more a year from now if a mortgage is necessary to purchase your next home.

5. It’s Time to Move On with Your Life

Look at the reason you are thinking about selling and decide whether it is worth waiting. Is the possibility of a few extra dollars more important than being with family; more important than your health; more important than having the freedom to go on with your life the way you think you should?

You already know the answers to the questions we just asked. You have the power to take back control of your situation by putting the house on the market today. The time may have come for you and your family to move on and start living the life you desire. That is what is truly important.

Are you condisering selling your home? Give us a call, we would love to help you home to obtain top dollar for your home in today's marketplace.

?-Steve and Sandra

Steve Hill and Sandra Brenner

Windermere Real Estate/FN

122502 Greenwood Ave N

Seattle WA 98133

call/text: 206-769-9577

email: stevehill@windermere.com

Check out these useful links:

BrennerHill.com

Best In Client Satisfaction

Windermere Housing Trends Newsletter

Our Preferred Lenders

George Runnels

Washington First Mortgage

WaFirstMortgage.com

call/text: 206-604-4545

Jackie Murphy

Cobalt Mortgage

CobaltMortgage.com

call/text: 425-260-6834

Should I Rent My House If I Can’t Sell It?

There has been a lot written about how buying a home is less expensive than renting one in most parts of the country. Rents are skyrocketing and homes are still at great prices. These two situations are also causing some sellers to consider renting their home instead of selling it. After all, a homeowner can get great rental income now and perhaps wait until house values increase even further before selling.

There has been a lot written about how buying a home is less expensive than renting one in most parts of the country. Rents are skyrocketing and homes are still at great prices. These two situations are also causing some sellers to consider renting their home instead of selling it. After all, a homeowner can get great rental income now and perhaps wait until house values increase even further before selling.

This logic makes sense in some cases. We at KCM believe strongly that residential real estate is a great investment right now. However, if you have no desire to actually become an educated investor in this sector, you may be headed for more trouble than you were looking for.

Before renting your home, you should answer the following questions to make sure this is the right course of action for you and your family.

10 Questions to Ask BEFORE Renting Your Home

1.) How will you respond if your tenant says they can't afford to pay the rent this month because of more pressing obligations? (This happens most often during holiday season and back-to-school time when families with children have extra expenses).

2.) Because of the economy, many homeowners can no longer make their mortgage payment. What percent of tenants do you think can no longer afford to pay their rent?

3.) Have you interviewed a few experienced eviction attorneys in case a challenge does arise?

4.) Have you talked to your insurance company about a possible increase in premiums as liability is greater in a non-owner occupied home?

5.) Will you allow pets? Cats? Dogs? How big a dog?

6.) How will you actually collect the rent? By mail? In person?

7.) Repairs are part of being a landlord. Who will take tenant calls when necessary repairs arise?

8.) Do you have a list of craftspeople readily available to handle these repairs?

9.) How often will you do a physical inspection of the property?

10.) Will you alert your current neighbors that you are renting the house?

Bottom Line

Again, renting out residential real estate historically is a great investment. However, it is not without its challenges. Make sure you have decided to rent the house because you want to be an investor, not because you are hoping to get a few extra dollars by postponing a sale.

Wondering if you should rent or sell? Give us a call, we can help guide you to a decision.

-Steve and Sandra

Steve Hill and Sandra Brenner

Best In Client Satisfaction

Windermere Real Estate

BrennerHill.com

call/text 206-769-9577

Our Preferred Lenders

George Runnels

Washington First Mortgage

WaFirstMortgage.com

call/text: 206-604-4545

Jackie Murphy

Cobalt Mortgage

CobaltMortgage.com

call/text: 425-260-6834