Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

Moving-Up? Do it NOW not Later

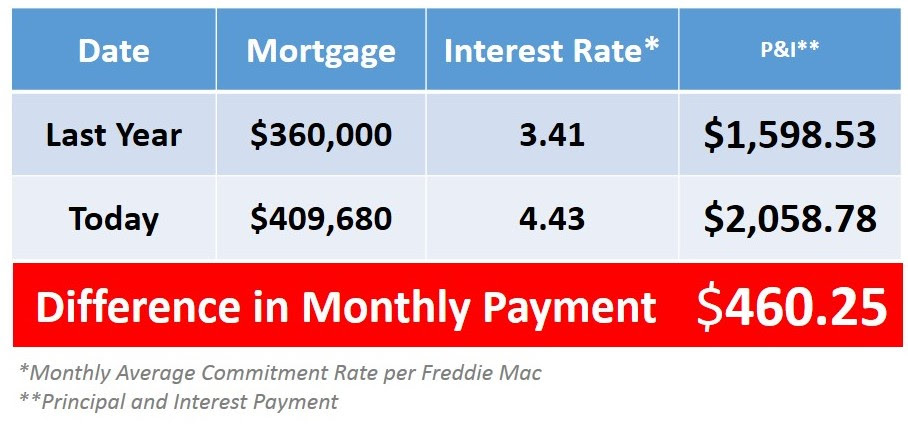

A recent study revealed that the number of existing home owners planning to buy a home this year is about to increase dramatically. Some are moving up, some are downsizing and others are making a lateral move. Another study shows that over 75% of these buyers will, in fact, be in that first category: a move-up buyer. We want to address this group of buyers in today’s blog post.

There is no way for us to predict the future but we can look at what happened over the last year. Let’s look at buyers that considered moving up last year but decided to wait instead.

There is no way for us to predict the future but we can look at what happened over the last year. Let’s look at buyers that considered moving up last year but decided to wait instead.

Assume they had a home worth $300,000 and were looking at a home for $400,000 (putting 10% down they would get a mortgage of $360,000). By waiting, their house appreciated by 13.8% over the last year (national average based on the Case Shiller Pricing Index). Their home would now be worth $341,400. But, the $400,000 home would now be worth $455,200 (requiring a mortgage of $409,680).

Here is a table showing what additional monthly cost would be incurred by waiting. If you have questions about current mortgage rates, be sure to contact one of our preferred lenders below.

-Steve and Sandra

Steve Hill and Sandra Brenner

Steve Hill and Sandra Brenner

Windermere Real Estate/FN

Seattle-Northwest

122502 Greenwood Ave N, Suite A

Seattle WA 98133

call/text: 206-769-9577

email: stevehill@windermere.com

Check out these useful Home Search Apps:

Windermere for iPad

Windermere for Android

Check out these useful links:

BrennerHill.com

Best In Client Satisfaction

Seattle Real Estate Statistics

Windermere Housing Trends Newsletter

Our Preferred Lenders

George Runnels

Washington First Mortgage

WaFirstMortgage.com

call/text: 206-604-4545

Jackie Murphy

Cobalt Mortgage

CobaltMortgage.com

call/text: 425-260-6834

Mortgage Rates Projected to Rise as Tapering Continues

It is projected that if the Fed continues to cut back on bond purchases that long term mortgage rates would start to climb. Many experts felt that Janet Yellen, who replaced Ben Bernanke as Fed Chair, was going to be less inclined to continue tapering bond purchases at the level established.

It is projected that if the Fed continues to cut back on bond purchases that long term mortgage rates would start to climb. Many experts felt that Janet Yellen, who replaced Ben Bernanke as Fed Chair, was going to be less inclined to continue tapering bond purchases at the level established.

However, in her testimony in front of the Financial Services Committee last week, Yellen made it quite clear that she will in fact continue the current pace of tapering:

“In December, the Committee judged that the cumulative progress toward maximum employment and the improvement in the outlook for labor market conditions warranted a modest reduction in the pace of purchases, from $45 billion to $40 billion per month of longer-term Treasury securities and from $40 billion to $35 billion per month of agency mortgage-backed securities. At its January meeting, the Committee decided to make additional reductions of the same magnitude. If incoming information broadly supports the Committee's expectation of ongoing improvement in labor market conditions and inflation moving back toward its longer-run objective, the Committee will likely reduce the pace of asset purchases in further measured steps at future meetings.”

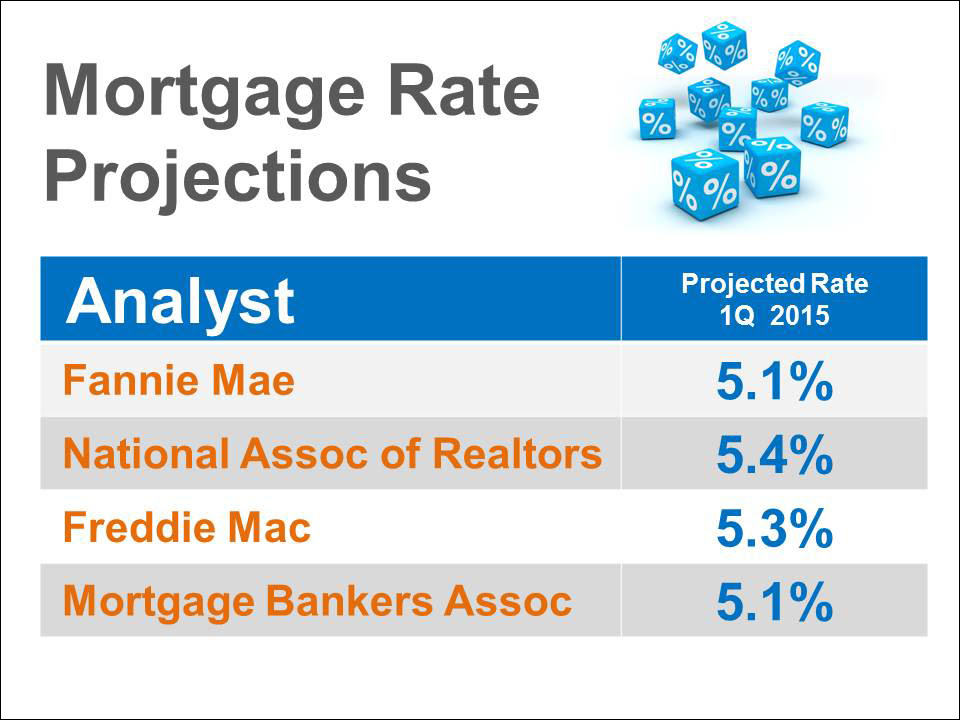

What does that mean to a prospective purchaser? Currently, Freddie Mac’s 30 year rate is at 4.28%. Here are the projected interest rates for this time next year:

If you have question about mortgage rates, give us a call, text or email. We will be happy to answer any of your real estate related questions.

?-Steve and Sandra

Steve Hill and Sandra Brenner

Windermere Real Estate/FN

Seattle-Northwest

122502 Greenwood Ave N, Suite A

Seattle WA 98133

call/text: 206-769-9577

email: stevehill@windermere.com

Check out these useful Home Search Apps:

Windermere for iPad

Windermere for Android

Check out these useful links:

BrennerHill.com

Best In Client Satisfaction

Seattle Real Estate Statistics

Windermere Housing Trends Newsletter

Our Preferred Lenders

George Runnels

Washington First Mortgage

WaFirstMortgage.com

call/text: 206-604-4545

Jackie Murphy

Cobalt Mortgage

CobaltMortgage.com

call/text: 425-260-6834

30-year mortgage rate steady at 4.57%

WASHINGTON (AP) — Average U.S. rates on fixed mortgages held steady this week, hovering near two-year highs. But rates could change quickly next week when the Federal Reserve addresses its bond purchase program.

WASHINGTON (AP) — Average U.S. rates on fixed mortgages held steady this week, hovering near two-year highs. But rates could change quickly next week when the Federal Reserve addresses its bond purchase program.

Mortgage buyer Freddie Mac said Thursday that the average rate on the 30-year loan was unchanged from last week at 4.57%, just below the two-year high of 4.58% reached Aug. 22.

The average on the 15-year fixed mortgage held at 3.59%. The two-year high of 3.60% was hit on Aug. 22.

Long-term mortgage rates have risen more than a full percentage point since May, when Chairman Ben Bernanke first signaled that the Fed could reduce its bond purchases this year. The purchases have been intended to keep long-term loan rates extremely low.

Most analysts expect the Fed to decide at its meeting next week to scale back its bond purchases.

Even with the recent gain, mortgage rates remain low by historical standards. But higher rates have spurred some homebuyers to close deals quickly and could slow the market's momentum if they continue to rise.

Mortgage rates have been rising because they tend to track the yield on the 10-year Treasury note. The yield has climbed 1.3 percentage points in the past four months as bond traders have anticipated that the Fed will slow its bond buying.

The 10-year note's rate was 2.92% on Wednesday, down from 2.97% Tuesday but up from 2.89% a week earlier.

To calculate average mortgage rates, Freddie Mac surveys lenders across the country on Monday through Wednesday each week. The average doesn't include extra fees, known as points, which most borrowers must pay to get the lowest rates. One point equals 1% of the loan amount.

The average fee for a 30-year mortgage rose to 0.8 point from 0.7 point. The fee for a 15-year loan was steady at 0.7 point.

The average rate on a one-year adjustable-rate mortgage fell to 2.67% from 2.71%. The fee declined to 0.4 point from 0.5 point.

The average rate on a five-year adjustable mortgage dipped to 3.22% from 3.28%. The fee was unchanged at 0.5 point.

Curious about mortgage rates or refinancing? Give us a call, we are happy to help.

Steve Hill and Sandra Brenner

Best In Client Satisfaction

Windermere Real Estate

BrennerHill.com

call/text 206-769-9577

Our Preferred Lender:

George Runnels

Washington First Mortgage

WaFirstMortgage.com

call/text: 206-604-4545

Should I Wait for Interest Rates to Come Back Down?

Above is a graph of the movement of the 30 year fixed mortgage rate since the beginning of 2012.

Above is a graph of the movement of the 30 year fixed mortgage rate since the beginning of 2012.

Some buyers are waiting to see if interest rates will come back down before making a decision about buying a home. Though no one can guarantee where rates will be in a few months, we don’t believe waiting is a good strategy.

Most experts believe rates may actually move higher. The Mortgage Bankers Association, Fannie Mae, Freddie Mac and the National Association of Realtors are in unison projecting that rates will continue to climb.

With home prices increasing and interest rates projected to also increase, the cost of buying a house could quickly increase rather dramatically.

If you are searching for today's best rates on home mortgages, give George Runnels at Washington First Mortgage a call, he can find you the best terms for new or refinancing a home loan. 206-604-4545

Curious about interest rates and how they can affect your purchasing power? Give us a call or text to learn more.

Steve Hill and Sandra Brenner

Best In Client Satisfaction

Windermere Real Estate

call/text 206-769-9577

BrennerHill.com

The COST of a Home: Last Year, This Year & Next Year

The cost of a home is determined mainly by two components: price and mortgage rate. Today, we want to show how the monthly cost of purchasing a median priced home has changed over the last twelve months and how it might change over the next twelve months. For the first two examples, we will be using the National Association of Realtors’ (NAR) Existing Home Sales Report to establish median price and Freddie Mac’s Primary Mortgage Market Survey to establish mortgage rate. We also assumed a 20% down payment in all examples.

The cost of a home is determined mainly by two components: price and mortgage rate. Today, we want to show how the monthly cost of purchasing a median priced home has changed over the last twelve months and how it might change over the next twelve months. For the first two examples, we will be using the National Association of Realtors’ (NAR) Existing Home Sales Report to establish median price and Freddie Mac’s Primary Mortgage Market Survey to establish mortgage rate. We also assumed a 20% down payment in all examples.

LAST YEAR

The median priced home in the country was selling for $187,800. The 30-year fixed mortgage rate was at 3.5%. Here is what it would cost to buy a home last year:

TODAY

The median priced home in the country is selling for $213,500. The 30-year fixed mortgage rate is at 4.5%. Here is what it would cost a purchaser to buy a home today:

The monthly cost increased by: $190.78!

NEXT YEAR

Projecting into the future in real estate can be rather tricky. To establish future pricing, we depended on the over 100 housing experts surveyed for the Home Price Expectation Survey who called for an approximate appreciation rate of 5% over the next twelve months. For the interest rate, we took the average of the projections from the Mortgage Bankers’ Association, Freddie Mac and Fannie Mae. Here is what these experts project will be the approximate cost of a home a year from now:

The monthly cost will increase by about: $97.32!

Bottom Line

From a financial perspective, why wait if you are thinking about buying?

Article courtesy of KCM Blog

Posted: 26 Aug 2013 04:00 AM PDT

If you are considering buying a new home, get off the fence! Waiting will only cost you money. Give us a call, we are ready to help you find your new home.

Steve Hill and Sandra Brenner

Best In Client Satisfaction

WIndermere Real Estate

Call/Text: 206-769-9577

Total Increase a Buyer May Pay if They Wait

Earlier in the week, we explained that experts have projected that U.S. home prices will appreciate by approximately 5% in 2013. We also revealed the Mortgage Bankers Association, Fannie Mae and the National Association of Realtors have all projected that the 30-year mortgage rate will be at least 4% by the end of 2013. If we assume that prices and interest rates will rise as projected, here is the monthly difference a buyer may pay if they wait a year.

Earlier in the week, we explained that experts have projected that U.S. home prices will appreciate by approximately 5% in 2013. We also revealed the Mortgage Bankers Association, Fannie Mae and the National Association of Realtors have all projected that the 30-year mortgage rate will be at least 4% by the end of 2013. If we assume that prices and interest rates will rise as projected, here is the monthly difference a buyer may pay if they wait a year.